Revisiting the Legal Publishing Market

The shrinking of options in the legal publishing world has been a pretty constant theme in my years in law librarianship. Just when you think it has settled down a little, along comes another consolidation/merger/takeover.

In December it was announced that Bloomsbury Press had bought RELX law assets. These include 6 Family Law titles held by LexisNexis and Jordan Family Law publishing. This came about because Lexis (ie, RELX) has purchased Jordan’s Family Law, and part of the deal with the CMA was that some titles be sold elsewhere to ensure competition. J

It’s a bit like ping pong match as you watch these ‘assets’ move around. It doesn’t seem that long ago that Jordan’s took its Family Law titles away from the Lexis platform and placed them on their own platform, thus adding a new cost to our already constrained budgets. Titles that had once been part of the aggregated package in the Lexis offering were now an additional purchase if you were to keep your family lawyers happy.

It’s not yet known what Bloomsbury will do with the products, but their track record makes us a little wary. When they bought Hart Publishing in 2013 Bloomsbury stopped honouring the discounts that had previously been in place between Hart and academic institutions, and left libraries scrambling to find funds to retain core Hart titles.

This is only one story among many, of course. What are seen as core academic tools (certain books and journals and law reports) by librarians, are mere assets to publishing houses and are often traded as such. We, as customers, have to make the adjustments. We have to keep track of new vendor details, juggle budgets to accommodate the inevitable price hikes, and maintain access to the core resources our users rely on in their teaching and research.

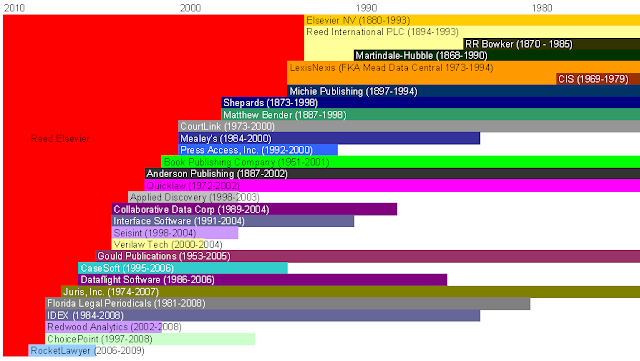

I once saw a timeline demonstrating publisher acquisitions and aggregations in the 1990s which showed how dozens of small, independent and often high quality legal publishers had been reduced to four or five large publishers through acquisition or merger or failure. It was one of those salutary heads up moments when you realise that there are forces at work out of your ken which beaver away in the background and change your world while you sleep. Because I have lost the original timeline wall chart, I went hunting and have located several more recent charts which help demonstrate the mergers graphically.

On the 3 Geeks and a Law blog, this chart shows the Reed Elsevier stable in 2010, as well as the Thomson Reuters collection. Sarah Glassmeyer’s updated chart of 2014 has the most recent overview of what has happened in the past 2 decades across the three largest legal publishers. In addition, there is a generalist overview across major academic publishers in this article of 2007 http://www.ulib.niu.edu/publishers

We know in our own jurisdictions that these changes happen regularly, such as the divestment by Wolters Kluwer of some of its assets in Canada and Russia to Lexis, or the purchase by Kluwer of Polish assets from Lexis and last year’s purchase of Loislaw by Fastcase, all ongoing evidence of this moveable landscape.

As customers, trying to keep track of your suppliers is adds to the work of the acquisitions staff. In most organisations, not least universities, accounting systems and procedures require a list of approved suppliers for purchasing. So each time we have a change of supplier, it requires that we not only change our records, we also have to go through a form filling exercise to have this new supplier approved by the purchasing department before we can pay any invoices. None of this is seamless, all of it is time consuming. It is only as I write this that I stop to think how very complicated and bureaucratic these enterprise-wide accounting systems have made our lives!

{kind=link}

{kind=link}

Hi Ruth.

Good points made, I believe and I tend to agree with you. You might also be concerned that Bloomsbury Professional may have existing contractual arrangements with both LexisNexis/Reed Elsevier and Thomson Reuters for the provision of legal content, so that, in effect, with the integration of Jordan Publishing Limited into Reed Elsevier and even allowing for the disposal of certain titles to Bloomsbury, access to legal content is further limited.

You will also be aware that in consequence of the acquisition some time ago by Thomson Reuters of PLC, that contractual arrangements by which Bloomsbury licensed content to PLC and therefore subsequently to Thomson Reuters, created a contractual relationship between Bloomsbury and Thomson Reuters. This is enhanced by the recent agreement by which Bloomsbury has agreed that a selection of Bloomsbury Publishing’s legal print titles are set to be distributed as e-books through Thomson Reuters’ professional e-reader ProView, see: http://www.thebookseller.com/news/thomson-reuters-and-bloomsbury-partner-provide-legal-e-books-316962.

It might reasonably be anticipated that the content in question may find its way, by means of licensing arrangements, back to LexisNexis as well as to Thomson Reuters.

My concern might be that effectively the vast majority of legal content, with its effect on pricing and customer choice, remains with or to an even greater extent than before, resides with the two market leaders, with Bloomsbury Professional performing the role of a small content acquirer and licensor to both. Despite the scrutiny of the Competition and Markets Authority in these matters, in real terms worst of the status quo may persist. Customer choice may therefore become more limited than before and this may have a detrimental effect on many of the other smaller legal and tax publishers that operate in the UK market.

Personally I envisage much more of the same, http://www.slaw.ca/2015/04/24/the-future-of-legal-publishing/, until the idea of a “legal publishing industry” all but disappears, with what is left being a minor function amid supply of back office and support services to only the largest firms. Nor would it be absurd to envisage Bloomsbury Professional/Hart as a future acquisition target, maybe of Thomson Reuters. My own next Slaw article, “A Most Ordinary Curriculum Vitae”, speculates on this.

How very labyrinthine – much more intricate than I realised. Well done jkeeping on top of it all, Robert! It becomes so daunting from the point of view of the librarian as intermediary between the reader (who does not care about who owns what, and thinks we are the evil ones denying them a resource) and the suppliers….

Fascinating post, Ruth. I haven’t had a chance to allow my thoughts to “marinate” long enough on this, but did want to offer up my own two-penneth on one aspect of the recent acquisition of Jordan Family Law by LexisNexis.

From the perspective of a law reporter, one particularly interesting aspect of that acquisition is the movement of law reporting “assets” from Jordan to LexisNexis and from LexisNexis to Bloomsbury Professional.

As I understand the transaction, LexisNexis have acquired the Family Law Reports (FLR) from Jordan, but have disposed of their own Family Court Reports (FCR) to Bloomsbury Professional in order to keep to CMA happy. So, we now have the leading family law series (the FLR) in the hands of LexisNexis and LexisNexis’ previous attempt to compete with Jordan (the FCR) in the hands of Bloomsbury.

In some ways, this may in fact result in a more meaningful augmentation in options rather than a shrinking of them. If Bloomsbury Professional get their heads down and develop the FCR to be capable of competing with the FLR (and I hope that they do), that means that family practitioners would have a choice between to semi-decent law reporting platforms: FLR on LexisNexis or FCR through Bloomsbury. The latter will invariably cost less to the consumer than the former.

During my time at ICLR, I have observed a strange paradox in the legal information market on the consumer end. On the one hand, the consumer requires choice and value for money. On the other hand, the consumer also appears to have a desire to source as much information as possible through a single online outlet (normally, this means Westlaw or LexisNexis). The preference for a single outlet is understandable, because as a consumer you only need to deal with one vendor, one set of prices and one platform upon which to train the end users.

The problem is that the urge for a single solution is completely incompatible with any urge to achieve choice and value in the legal information market.

I believe that the consumer of the market has far more power than it to realises to drive legal publishing towards choice and value. But, the exercise of that power depends on a more robust and thoughtful appraisal of what information consumers really require and a where that information can be sourced from.

Depending on the depth of the research being done the idea of different vendor platforms and hence varying skills and techniques required of each platform appears to be rather inefficient. Is this deliberate on the part of the vendors to cater to the traditional law firm culture of the billable hour? Having to choose between vendors seems to create a greater divide between have and have not law firms (big or small). What hasn’t been addressed is the impact that the inefficiency caused by having to use different platforms may have on access to justice. That is, is this inefficiency driving up/down legal services costs?