The Biz-Ification of Law

“Competitive markets are not much fun for sellers” – Richard Posner

It’s common knowledge that the billable hour is holding back the profession. Additionally, it’s clear that professional conduct rules insulate lawyers, prevent other professionals from getting involved, and stifle innovation. Yet, despite the billable hour still going strong and no changes in professional conduct rules, we are seeing an unprecedented boom in innovative legal services. It feels like something bigger must be going on.

Market cycles

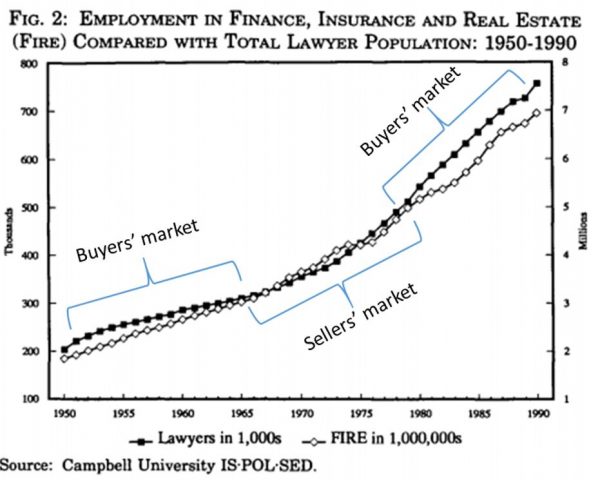

While the literal number of lawyers remains a significant factor, more important is its ratio to finance, insurance, and real estate (“FIRE”) employment. When banks and insurance companies lend more money, when businesses and individuals insure against more risk, and when real estate transactions grow, lawyers have plenty of work. As you can see in the chart below, for a long time the growth in lawyer numbers didn’t stray far from the ratio of about 9.43 FIRE employees (or the purchasers of legal services they represent) for every lawyer:

Even though people often complain about lawyers being insulated from competition it’s pretty clear that, for quite a while, lawyers generally didn’t stray too far from the rest of the economy. The supply and demand cycle functioned how one would expect: “As more legal work became available, more people decided to go to law school. As more lawyers became available, the value of their services declined”.

If this cycle were all that happened, we should expect the growing flurry of innovation to eventually go away. As the market corrected itself, things would eventually shift back into a sellers’ market. However, the sea change that actually appears to be happening seems outside the bounds of these typical market cycles.

Biz-ification

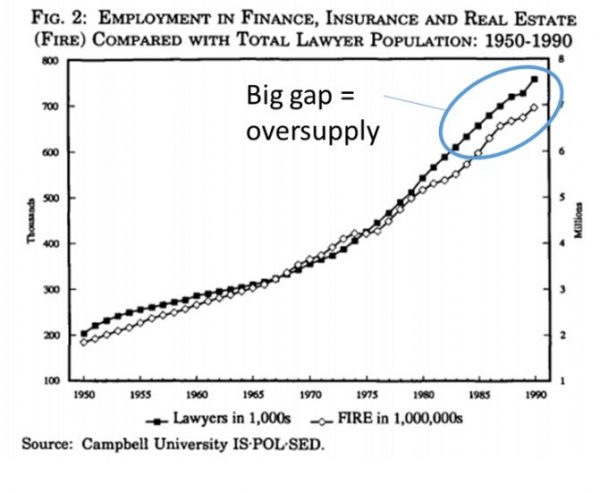

A large increase in the supply of lawyers should lead to the market correcting by supplying fewer lawyers. But what happens when law schools keep growing and new ones pop up while we’re already in a buyers’ market, and the demand for legal services slows down?

The ensuing lawyer logjam has led to extreme oversupply. As the market value of lawyers has diminished, we haven’t seen a corresponding reduction in the number of lawyers. Even though law the legal job market began to stagnate before the 2008 recession, new lawyers kept getting licenses. Eventually, the ratio became so different for so long that the market started to adjust to a new normal.

The number of legal jobs always fluctuates, but now the very nature of legal jobs is changing. The term “lawyer” continues to balkanize. And even if rules around self-regulation had used to keep access to legal services a scarce resource, there are now too many lawyers doing too many different things for such rules to be effective. As we move from a “profession” to an “industry”, we have entered “the biz-ification of law.”

Loss of market power

Lawyers who were not in firms moved into three areas that have each driven this biz-ification: in-house legal departments, legal out-sourcing companies (and ALSPs), and legal tech.

First, in-house lawyers propelled the biz-ification of law by massively lowering the cost and risk of switching firms. Companies used to rely on law firms to (1) diagnose what legal services they need, and (2) ensure the quality (both pre- and post-purchase) of the legal services they received. Because of these information asymmetries, shopping around for a better price was not worth the risk of losing a reliable law firm (sort of like finding a good mechanic). Full service firms evolved as a way to accommodate their clients’ concerns toward switching by efficiently monitoring referrals to specialized lawyers.

Yet when companies began to bring more lawyers in-house, they internalized theses diagnosis and quality control functions. Long-term relationships became less important – they were now more of a nice to have and less a method of managing one’s legal needs. Companies had acquired the ability to monitor the work of outside counsel, [1] which enabled them to bargain over price.

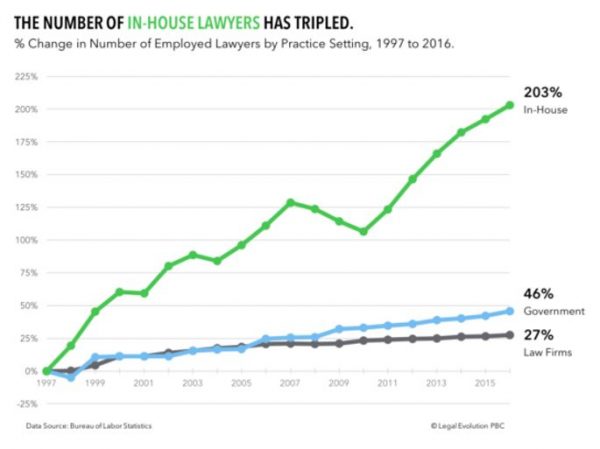

That ability not only drove prices down, it massively changed the market’s dynamics. In-house counsels began to select their own specialists. The rule became to hire lawyers, not firms. Some large companies have used as many as 700 law firms at one time. Take a minute to think about that stat. Now think about the power such a company must have to then cut ties with 680 of those firms in just six months. That requires cancelling relationships with 113 firms every month. That is the extreme power of just one (very large) company. It gets even worse for private practice when you consider that the number of in-house lawyers has tripled since 1997. It’s not an exaggeration to describe the current in-house revolution as tantamount to the “elimination” of lawyers’ market power.

Second, even after the expansion of in-house legal departments there are still just so many lawyers. This lawyer glut fueled the first wave of legal outsourcing (e.g. doc reviewers for eDiscovery). It also supplies lawyers to ALSPs. As buyers get even more options, it further dilutes the market power of law firms.

Lastly, many former lawyers have decided that, if they’re already resigned to working lawyer-esque long hours, they might as well have a stake in the overall success of what they’re working toward from the start. As more people join legal tech companies, they bring with them the necessary expertise to train AI systems, further complicating life for law firms.

The necessary ingredients for lawyers to maintain their identity as autonomous craftsmen have gone away. Though the below two graphs don’t cover the same time span, they do reinforce the importance that the supply/demand ratio has on the legal profession. I suspect that the gap between lawyers and FIRE employees has continued to widen. And I’m confident that the more the population of in-house lawyers grows, the less market power law firms will have.

A structural shift

The number of lawyers kept growing far beyond what a typical market cycle could sustain. There’s no one cause: perhaps because of a tragedy of the commons (law schools and law societies are both being incentivized to grow the number of lawyers), or the supply/demand feedback loop became too delayed. Regardless, extreme oversupply forced lawyers to find jobs outside of law firms, taking salaries that legal departments or legal companies were willing to pay. By internalizing diagnostic and quality control functions, companies lowered the cost of switching enough to drive the biz-ification of law. The current changes in the legal profession are not simply another buyers’ market. Law firms appear to be caught flat-footed. But it’s hard to blame them, given we’re witnessing an unprecedented structural shift.

Of course, lowered switching costs for companies has made law more transactional, but what else?

As businesses gain more market power, they will continue to demand more from their legal providers. Instead solving legal problems, businesses will want lawyers to solve “business challenges that raise legal issues.” This might feel like semantics, it’s worth thinking of the growing number of companies creating strategic partner programs to do just that. It’s also worth thinking about how much market power clients must now have to be able to pull competing law firms into a room and have them cooperate.

Not only will the legal services market change, but the legal job market will change as well. The historical continuum from lawyers as generalists, to specialists, to project managers will continue to splinter into new titles such as legal knowledge engineer, legal technologist, legal risk manager, etc. The identity of what it means to be a lawyer will become more amorphous, making it harder to regulate. Without the market power to resist it, legal work will become more multi-disciplinary. The shift toward multi-disciplinarity shows up in “lawyers who code” debates and the fact that more people than ever are going to law school not to become lawyers, but to “acquire transferrable skills”.

Lastly, legal regulators will struggle to stay relevant. Rules intended to protect buyers of legal services don’t seem to matter as much when the biggest buyers have already dropped any concerns over non-lawyer ownership in favour of ALSPs. Law firms themselves seem to be less concerned over maintaining a traditional partnership model as they add on roles such as VP and CTO. Lawyers who feel constrained by the rules have already found ways around them, just ask one Atrium co-founder: “[deregulation] has no impact on anything I think about.” And what do you do about people like Josh Browder who, despite having no legal training, is getting people out of parking tickets with his app? Legal regulatory bodies are already being forced to evolve and are exploring ways to deal with their changing role through regulatory sandboxes, commissioning reports, or trying to expand their scope.

What to do about it?

For starters, I wouldn’t put much confidence in professionalism rules protecting your practice. As one investor put it, “the market will continue to chip away at every part of a law firm that is not the pure provision of legal advice.” Because of extreme oversupply, any competition that had been dammed up by “non-lawyer” rules has now flowed right over top of it.

According to Clayton Christensen, there three potential strategies that law firms could use. Strategy #1 probably won’t work, which is to use marketing so that customers’ demand the performance improvements that you can provide. GC clients are sophisticated buyers and they have constant pressure to lower their legal spend, so I would be surprised if a law firm could convince them that they need more legal services. Either of the remaining two, “consciously pursued, can be successful,” though both require tough decisions.

Strategy #2 would retain the features of a typical law firm. Christensen’s advice is to “ascend sustaining tech into even higher tiers”. For law firms this means finding new areas of business or technology that will bring new legal problems with them. We see this strategy in the growing popularity of niches. The challenge with this strategy is that the firm must “ultimately [abandon] lower-tier customers” as those practice areas mature.

Strategy #3 is for those who want to march in lock-step with the given needs of their current customers. Christensen warns that “historically, this appears to have been difficult to do.” Indeed, David Maister also warns that following a practice area down its life cycle requires “transforming the fundamental nature of [the] firm.” The resources required for building greater expertise and for building greater efficiency do not align; and doing both under one roof will make it difficult to maintain a consistent company image. To address these difficulties, some firms have created off-shoots such as Osler Works or Seyfarth Lean.

Conclusion

From the 1930s to 50s, law was a buyers’ market and nearly all billing methods were value based. As the economy began to expand in the 1960s, much more legal work became available and we entered a sellers’ market. When the economy slowed down, the number of lawyers did not slow down with it. Oversupply was compounded by shrinking demand for legal services and still-growing law schools. Eventually, the value of lawyers dropped enough to entice lawyers into in-house roles, out-sourcing companies, and starting companies. These reactions to oversupply have precipitated a structural shift in the market for legal services, changing it from a profession to an industry – what I call the “biz-ification” of law.

The billable hour, the partnership model, and regulations over non-lawyer ownership certainly have effects, but there is clearly something bigger going on. The fact that past practices are less viable than they once were is not as interesting as asking why that is the case. The most immediate challenge is understanding why these changes are happening and adapting one’s mental models to fit that new reality.

_______________________

[1] As F. Leary Davis elaborates: In the 60s and 70s “clients did not have to worry about monitoring their lawyers. Since lawyers were so busy, they could not afford no ‘churn’ cases to build hours; doing so would prevent them from serving other needy clients and would be a detriment to the firm.”

Further evidence that, outside of lawyers, nobody cares about lawyer ownership anymore: Josh Browder’s DoNotPay Raises $4.6M from Silicon Valley Venture Firms

https://www.lawsitesblog.com/2019/07/donotpay-raises-4-6m-from-silicon-valley-venture-firms.html