“A Security Is What the Law Says It Is”: Legislative Breadth and Judicial Purpose in Canadian Securities Law

Canadian securities law has long resisted narrow or technical definitions of the term “security.” Instead, both legislatures and courts have embraced an intentionally expansive and purposive conception, one designed to capture a wide range of investment arrangements rather than a closed set of financial instruments. The oft‑invoked proposition that “a security is what the law says it is” reflects not interpretive casualness, but a deliberate regulatory strategy. Overbreadth in the statutory definition of “security” is not an accident of drafting; it is a conscious design choice that enables securities regulation to respond to evolving forms of capital formation and investment.

This article argues that Canadian securities legislation and jurisprudence work together to resist transactional formalism and regulatory circumvention. Legislatures employ open‑textured statutory language, while courts interpret that language purposively, focusing on economic substance rather than labels or private characterizations. The development of this approach can be seen in early judicial treatment of the definition of “security,” including the locus classicus test set by the Supreme Court of Canada in Pacific Coast Coin[i] and the more recent decision of the Alberta Court of Appeal in Stevenson[ii]. Together, these cases illustrate a coherent regulatory philosophy: securities law is concerned not with form, but with function and purpose.

The Statutory Architecture of “Security” in Canadian Legislation

Provincial securities statutes across Canada define “security” using inclusive, open‑ended language rather than exhaustive lists. While the specific wording varies by jurisdiction, the defining feature is consistency in technique. Legislatures enumerate familiar categories—such as shares, bonds, debentures, and notes—while also extending the definition to less formal instruments and arrangements. References to documents evidencing capital or indebtedness, profit‑sharing or participation interests, and investment contracts are common.

This drafting strategy is significant. By avoiding a closed or technical definition, legislatures preserve regulatory flexibility. New financial instruments and business models can be captured without constant statutory amendment. The definition of “security” thus functions not merely as a classificatory provision, but as a gateway into the regulatory regime. Once an arrangement is characterized as a security, the full apparatus of disclosure, registration, enforcement and other regulatory requirements becomes applicable.

The breadth of the definition also reflects the preventive and protective purposes of securities legislation. Securities law is not designed solely to police traditional capital markets, but to protect investors from informational asymmetries and abusive practices wherever they arise. A narrow definition would invite regulatory arbitrage, allowing promoters to structure transactions to evade oversight. Open‑textured statutory language minimizes that risk.

Overbreadth is a Feature, not a Flaw

Critics sometimes view broad statutory definitions as imprecise or over‑inclusive. In the context of Canadian securities law, however, overbreadth is best understood as a feature rather than a flaw. Securities regulation is inherently forward‑looking. It must anticipate financial innovation and respond to schemes that may not yet exist at the time of drafting.

Deliberate over‑inclusiveness serves this purpose. By casting a wide definitional net, legislatures signal that the focus of regulation is not the technical form of an instrument, but its economic function. The question is whether an arrangement involves the investment of capital with an expectation of profit, accompanied by risks that justify regulatory protection. This approach in statutory definition is particularly beneficial in the context of digital assets. Absent this feature, most digital assets would escape classification as securities, leaving regulators unable to exercise effective oversight. This would necessitate frequent legislative amendments, requiring securities regulators to repeatedly approach the Legislature for changes—an impractical approach given the dynamic and innovative nature of capital markets.

This approach stands in contrast to form‑driven or transactional conceptions of securities law, which risk becoming obsolete as markets evolve. Canadian legislatures have consistently chosen adaptability over precision, trusting courts to apply the definition purposively and contextually rather than mechanically.

Judicial Interpretation: Substance Over Form

Canadian courts have largely vindicated the legislative choice of breadth by adopting an interpretive approach that emphasizes substance over form. Courts routinely reject attempts by parties to contract out of securities regulation through characterization or structural design. Labels chosen by the parties—such as “private agreement,” “promissory note”, “membership interest,” or “joint venture”—are not determinative.

Judicial resistance to formalism manifests in several ways. Courts have rejected arguments that a transaction falls outside securities legislation merely because it is private or bespoke. They have declined to accept re‑labelling strategies designed to avoid regulatory scrutiny. Most importantly, courts have focused on the economic reality of the arrangement, asking whether it functions as an investment vehicle rather than whether it conforms to a traditional category.

A crucial doctrinal feature of this approach is the treatment of what constitutes a “security” as a question of law rather than a question of contract. By framing the issue this way, courts promote consistency and coherence across cases. The meaning of “security” does not fluctuate based on the intentions or descriptions of the parties but is anchored in statutory purpose and judicial interpretation.

Pacific Coast Coin: Supreme Court Confirmation of Regulatory Purpose

The Supreme Court of Canada’s decision in Pacific Coast Coin represents a definitive affirmation of the expansive, purposive interpretation of “security.” In this case, the Court situates the definition of “security” squarely within the broader objectives of investor protection and market integrity.

Rather than approaching the definition as a technical taxonomy, the Court emphasizes legislative intent and regulatory purpose. The decision underscores that securities legislation is designed to prevent harm before it occurs, not merely to remedy wrongdoing after the fact. Narrow or formalistic interpretations would undermine this preventive function. The Court set the following criteria used to determine when a scheme constitutes an “investment contract” under securities law:

- Investment of Money – Participants must contribute money (or money’s worth) into the scheme.

- Common Enterprise – The fortunes of investors must be interwoven with those of the promoter or other investors. This can include pooling of funds or a functional interdependence between investor and promoter.

- Expectation of Profit – Investors must enter the arrangement with the expectation of profit.

- Profit to Come Significantly from the Efforts of Others – The expected profit must depend primarily on the efforts, skill, or expertise of the promoter or a third party, not the investor.

- Substance Over Form – Courts look at the economic reality of the arrangement, not its label or formal structure.

Pacific Coast Coin was significantly influenced by the U.S. Supreme Court’s decision in SEC v. Howey[iii], but the Canadian Supreme Court adapted and expanded the U.S. approach to fit Canadian securities law. The language of the U.S. Howey test originally required profit to emanate solely[iv] from the efforts of others for a scheme to be deemed an investment contract. In contrast, Pacific Coast Coin requires the significant effort of others. In essence, Pacific Coast Coin while inspired by the core logic of Howey, reshaped it into a more flexible, substance‑focused test, with added determinative leverage. It is noteworthy that the requirement in the U.S. was replaced by the essential managerial effort requirement in latter cases[v].

Pacific Coast Coin also sends a clear signal that avoidance strategies will not be rewarded. By reinforcing the importance of substance over form, the Court discourages promoters from structuring transactions to skirt regulatory obligations. The decision confirms that definitional breadth is essential to effective securities regulation and not an interpretive anomaly to be corrected.

Stevenson: Sustaining Judicial Signals of an Expansive Approach

The decision in Stevenson illustrates how courts engage with the statutory definition of “security”. While the factual and doctrinal specifics of the case can be developed in greater detail elsewhere, its analytical significance lies in the court’s methodology.

In Stevenson, the court demonstrated a willingness to look beyond the parties’ descriptions of their arrangement and to assess its economic substance. Rather than treating the transaction as immune from securities regulation based on its form or context, the court examined the nature of the interest being offered and the expectations of the participants.

The reasoning in Stevenson aligns closely with the broader legislative purpose of securities law. The case reflects an understanding that the statutory definition of “security” is designed to be elastic, and that judicial interpretation must preserve that elasticity.

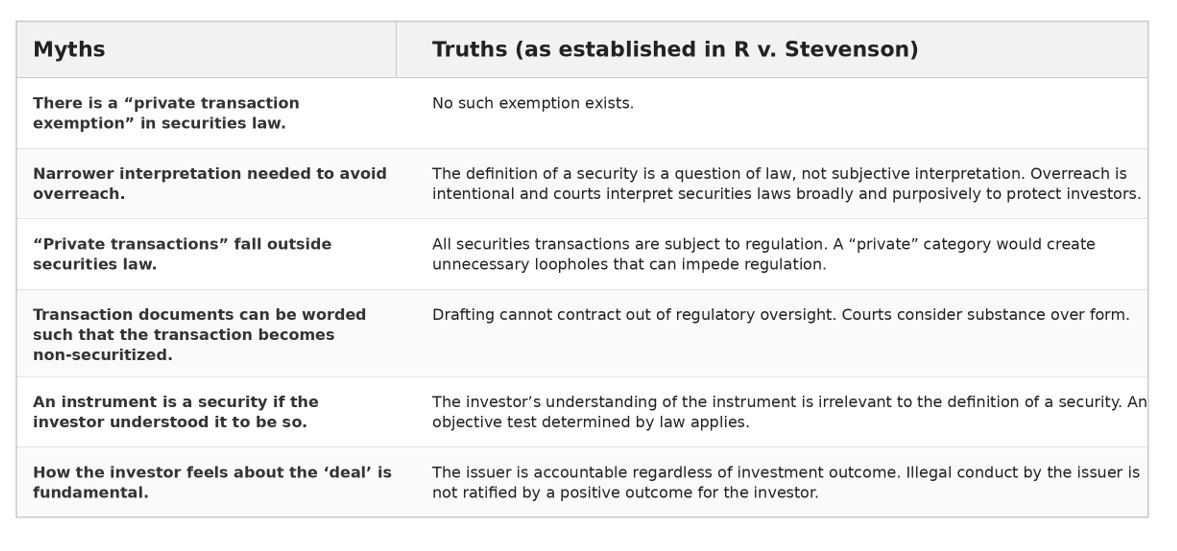

Myths vs. Truths About the Definition and Nature of a “Security”

Stevenson decisively dismantled several recurring arguments advanced in attempts to constrict the statutory definition of a “security.” The Court’s reasoning exposes these misconceptions and reaffirms the key legal principles, which are summarized in the table below.

The Definition of “Security” as a Tool of Regulatory Adaptability

Taken together, statutory drafting and judicial interpretation reveal that the definition of “security” functions as a dynamic regulatory instrument. It allows securities law to adapt to financial innovation, evolving business models, and hybrid investment schemes that defy traditional categorization.

This adaptability is particularly important in an era of rapid financial change. New technologies, unconventional financing arrangements, and novel asset classes continually test the boundaries of existing regulatory frameworks. An expansive definition, coupled with purposive interpretation, ensures that securities law remains effective without requiring constant legislative intervention.

Courts’ reluctance to narrow the definition preserves the integrity of the regime. By maintaining a broad gateway into securities regulation, courts support the legislature’s preventive and protective objectives and reinforce public confidence in capital markets.

Conclusion: Regulatory Purpose Over Transactional Formalism

Canadian securities law embraces an intentionally broad conception of “security.” This breadth reflects a principled commitment to substance, consistency, and investor protection rather than a failure of statutory precision. Legislatures have chosen open‑textured definitions to preserve regulatory flexibility, and courts have responded with purposive interpretations that resist formalism and evasion.

The decisions in Stevenson and Pacific Coast Coin exemplify this approach at different stages of the jurisprudence. Together, they demonstrate judicial fidelity to legislative purpose and confirm that overbreadth in the definition of “security” is not merely tolerated, but essential. In Canadian securities law, a security is indeed what the law says it is—and what regulatory purpose requires it to be.

Disclaimer:

The views and opinions expressed by the authors of this article are solely theirs and do not necessarily reflect the those of their employer and/or colleagues.

— Ronke Balogun and Solomon Ngoladi

_________________________

[i] Pacific Coast Coin Exchange v. Ontario Securities Commission, [1978] 2 S.C.R. 112

[ii] R. v Stevenson, 2017 ABCA 420

[iii] SEC v. Howey Co., 328 U.S. 293 (1946)

[iv] Justin Henning, “The Howey Test: Are Crypto-Assets Investment Contracts?” (2018) 27:1 University of Miami Business Law Review 68. – The main reason for the change from solely to essential managerial efforts was due to the “policy of affording broad protection to the public and the U.S. Supreme Court’s admonition that the definition of securities should be a flexible one”.

[v] SEC v. Glenn W. Turner Enterprises, Inc. is 474 F.2d 476 (9th Cir. 1973); Hocking v. Dubois, 885 F.2d 1449 (9th Cir. 1989)

Start the discussion!